Cash and Expense Management

Household payments are an operation. We run them like one.

Property managers, household staff, trust attorneys, art conservators — each invoice with its own approval chain, its own format, its own urgency. Some require wires. Some require discretion. All of them need to settle in the books.

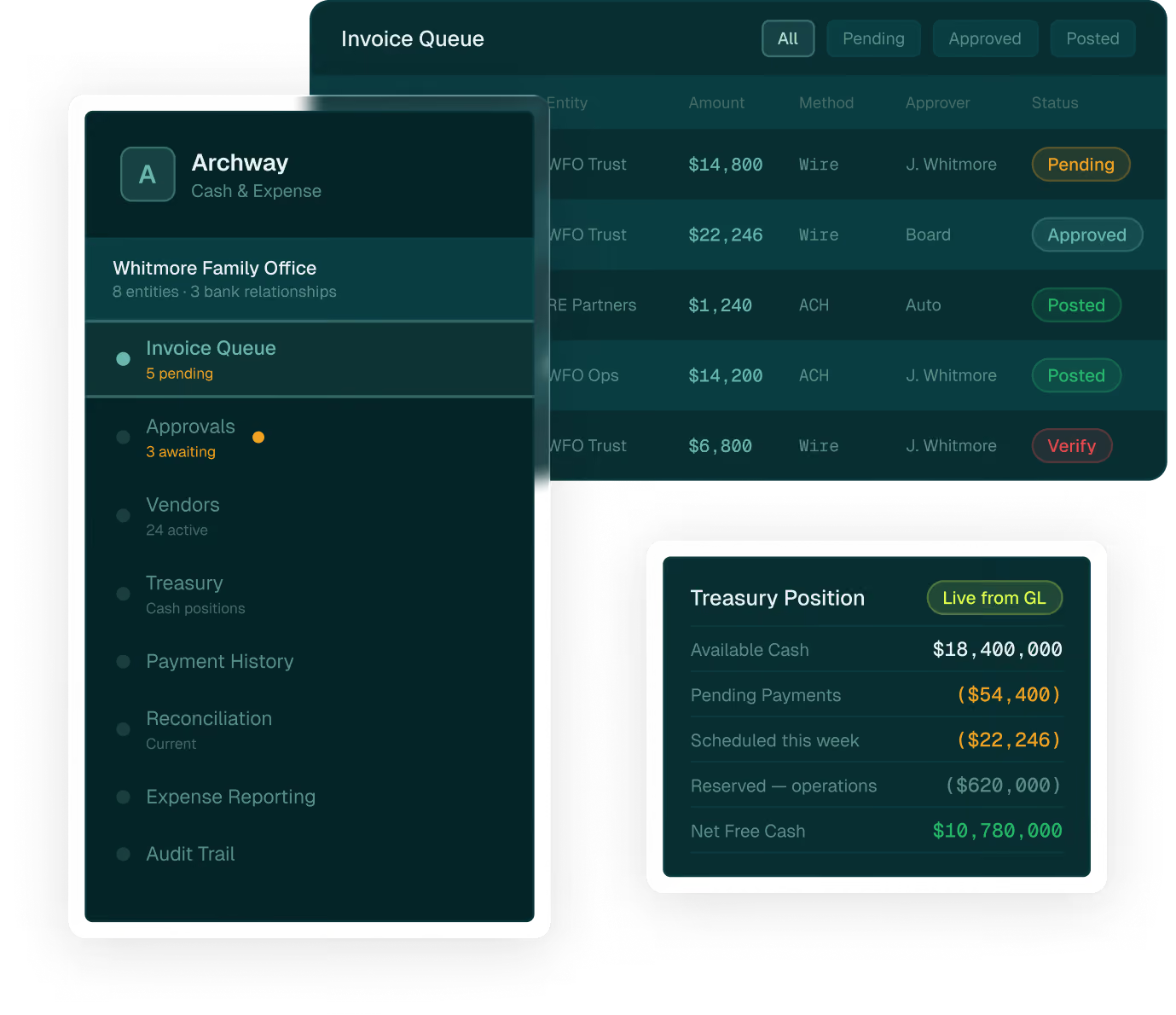

Archway runs cash and expense management on the same general ledger that holds the household's book of record. Every payment posts as a journal entry the moment it clears. No separate system. No reconciliation gap.

The problem we're solving

Bill pay only gets attention when something goes wrong.

By the time the principal calls about a missed payment, the problem has already compounded. A late fee. A damaged vendor relationship. A credit issue that takes months to resolve. The payment environment for a principal household isn't complex in theory, it's complex in practice, every day, across every entity, every bank account, every jurisdiction.

Property managers, household staff, trust attorneys, tax advisors, medical providers, luxury asset maintenance, each with its own invoice format, approval chain, payment method and urgency. Each payment has to come from the right entity, the right account, and has to be verified before it moves. A vendor impersonation scheme, a spoofed email, a fraudulent banking change request, is indistinguishable from a legitimate instruction if the controls aren't built into the process itself.

Most family offices run this on spreadsheets, email approvals, and a handful of staff who hold the institutional knowledge. When someone leaves, the process goes with them. When invoice volume grows, the process breaks. When a fraudster targets the household, informal controls aren't enough.

The deeper problem is structural. Bill pay, treasury and accounting are three functions that have to work together. Funds availability checked before payment, every payment posted to the general ledger the moment it clears, the audit trail complete and defensible. When those three functions run on separate systems, the coordination happens by email and reconciliation. That's where errors enter and oversight breaks down.

How it works

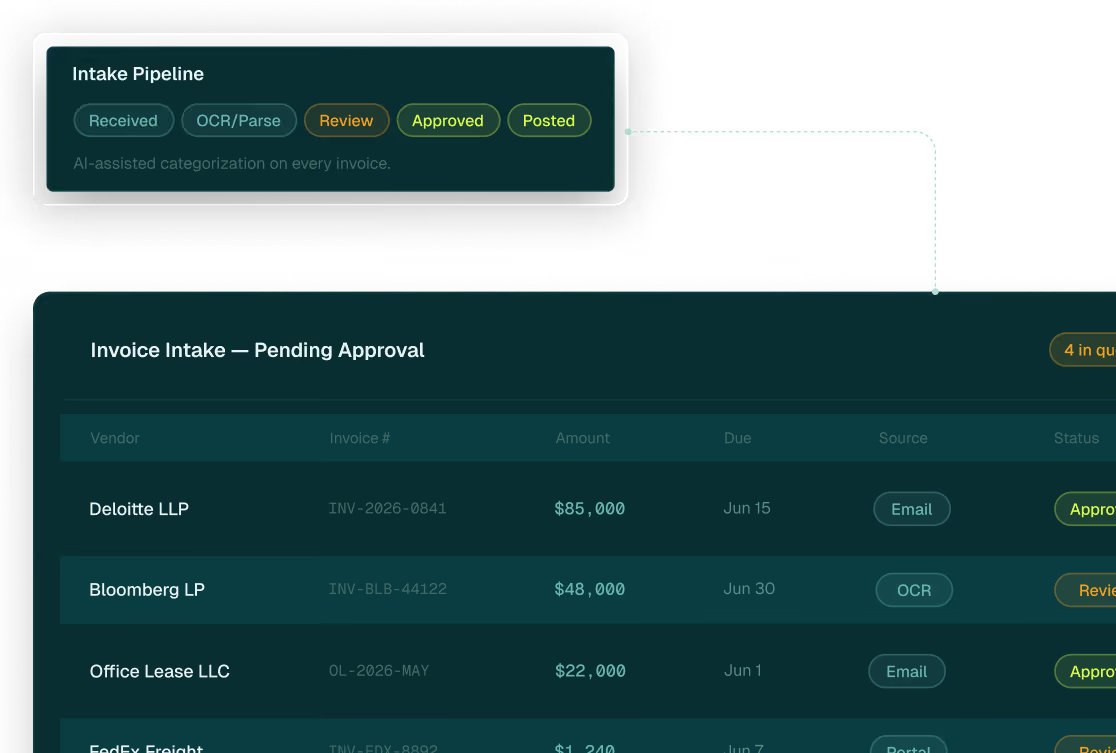

Invoice to journal entry. One system, end to end.

Every payment processed through Archway runs on the same general ledger that holds the household's book of record. Invoice intake through payment execution through reconciliation. One operation, no handoff between systems, no manual reconciliation step at month end.

Three ways to run cash and expense management

The model changes who handles the operations. The audit trail doesn't change.

Every household runs on the same platform, the same general ledger, the same book of record regardless of how they choose to deploy. The three models reflect different operational arrangements, not different tiers of service.

Technology

Your team runs cash and expense management on the platform. Archway provides the infrastructure.

Your controller or household ops team manages invoice intake, approval routing, payment creation and reconciliation through the Archway Platform — with full access to every capability the platform carries. Archway provides implementation, ongoing platform support and a dedicated client team. The work stays in-house. The infrastructure is ours.

Outsourced

Archway's team runs the operation end to end. Your household retains full visibility.

Invoices arrive at Archway. Our accountants and bookkeepers capture, route, verify, process and reconcile with discretion treated as a baseline operating requirement. The principal sees the deliverables. The audit trail is available in real time. The book of record is yours. The operational burden isn't.

Hybrid

Your team runs what makes sense to run in-house. Archway runs the rest.

The division is wherever the household wants it. Your team handles recurring payments, Archway handles complex transfers. Because both teams work on the same general ledger, there is no handoff, no version gap, no reconciliation step between what your team produces and what Archway produces.

Who runs on Archway

Four audiences, one operation. The discretion doesn't change.

Single family offices, multi-family offices, private banks and private fund managers all run cash and expense management on the same platform — same general ledger, same audit trail, same discretion. The brand on the deliverable and the team handling the keystrokes vary by model.

Clients stay for the team

"Outsourcing bill pay and a portion of our entity accounting to Archway has let us run a leaner internal team without giving up timeliness or control. Because the platform and services sit with the same firm, our staff isn't the coordinator between two vendors."

Single Family Office

·

Chief Investment Officer

FAQ's

What reporting evaluators ask about the platform.

How is Archway different from standalone bill pay tools and outsourced-only providers?

Archway combines cash and expense workflows, accounting, reporting, and operating support within one platform and service model. For families and advisors managing complex household operations, that connection can reduce handoffs between payment activity, documentation, approvals, and accounting records.

How does Archway integrate with our existing banking relationships?

Archway works with the banks the household already uses, including domestic and international banking relationships. Wires, paper checks, ACH transactions, and international transfers are issued through the household's own banking accounts. There is no need to move banking relationships.

How do you handle vendor confidentiality and staff payroll privacy?

Archway's cash and expense team operates under strict confidentiality protocols. Vendor relationships, staff compensation, and recipient details are accessible only to those with role-based access for that household. The audit trail is captured and reviewable. Discretion is a baseline operating requirement, not a feature.

How is pricing structured?

Pricing is based on the scope of the engagement, invoice volume, complexity of approval workflows, and services included. It is not per transaction. Specific pricing is provided after an initial conversation and scoping process.

How do you handle fraud prevention and vendor verification?

Vendor settlement instructions are maintained and verified before payment execution. Archway's verification protocols are embedded in the workflow to help reduce risks such as business email compromise, vendor impersonation, and unauthorized payment changes. Maker-checker controls on payments help ensure proper authorization before funds move.

How does cash and expense management connect to the accounting book of record?

Payments processed through Archway post to the general ledger, the same ledger that supports the accounting book of record. This connects cash and expense workflows with the books and helps reduce the need to reconcile activity across disconnected payment and accounting systems.

Start the conversation

The complexity doesn't resolve itself. But the right operation makes it manageable.

Tell us where the friction is — the approval chains, the vendor relationships, the payments that take too long or carry too much risk. We've seen it before. We'll come to the conversation with a point of view, not just a demo.

PERSPECTIVE

Reading for Fund Managers and Family Offices